Essential Integrations to Optimize Efficiency

In today’s competitive market, the success of financial institutions (FIs) heavily relies on their ability to process loan applications swiftly and efficiently.

To do so, financial institutions have started leveraging modern technologies. FIs today are majorly focused on improving and automating operational processes, especially with respect to Loan Origination Systems (LOS).

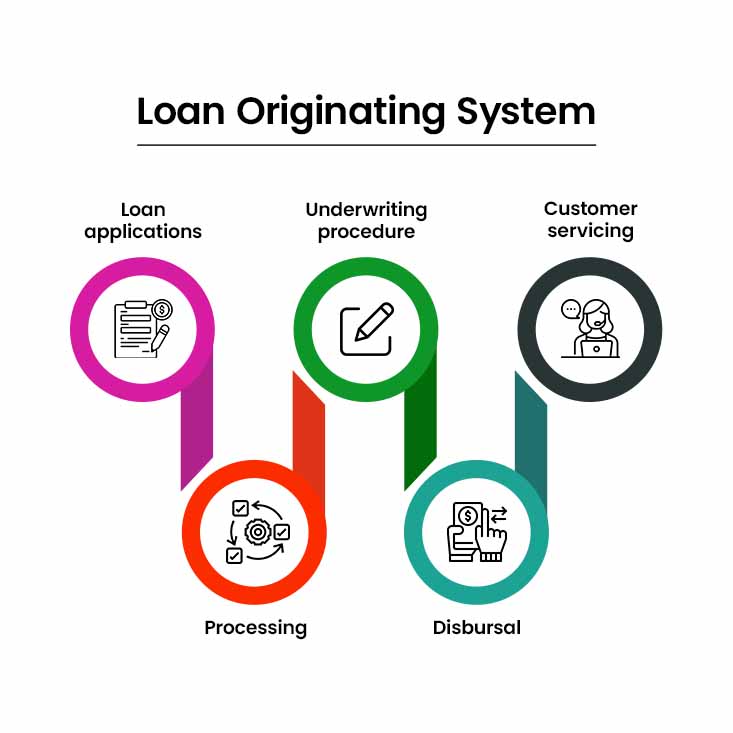

Here’s what a standard LOS looks like:

How A Loan Origination System Can Help Streamline Your Lending Process

LOS plays a vital role in this process, but to truly optimize efficiency and deliver an exceptional customer experience it is crucial to integrate various tools and services in it which will help in improving operational intelligence.

We, at Nitor Infotech will help you transform your lending process to better-informed, streamlined lending decisions.

In this blog, we will explore ten essential integrations required for a modern loan origination system, helping lenders streamline their operations and stay ahead of the competition.

So, without any further ado, let’s get started!

1. E-Signature Integration:

The days of handling physical paperwork are long gone. Integrating an e-signature solution into your loan origination system enables borrowers:

- To digitally sign documents

- Accelerate the application process

- Eliminate the need for manual document handling

This integration ensures secure and legally binding transactions while reducing operational costs and environmental impact.

A couple of examples of this would be DocuSign and Adobe Sign.

2. Credit Reporting Agencies:

Access to accurate credit information is essential for evaluating loan applicants. Integrating with reputable credit reporting agencies allows FIs to

- Access authentic data

- Obtain up-to-date credit scores and histories, giving them, as lenders, valuable insights into a borrower’s financial health

- Make informed decisions and mitigate the risk of defaults

Some examples of these agencies are CIBIL and CRISIL.

3. Income Verification Services:

To assess a borrower’s ability to repay a loan, income verification is vital. Integrating with income verification services, FIs can

- Enable lenders to verify an applicant’s income quickly and accurately

- Reduce the risk of fraud and ensure that the loans are offered responsibly

A few examples of this would be income tax certificate analysis and bank statements demonstrating regular income.

4. Bank Account Verification:

Streamline the verification of a borrower’s bank account details by integrating with banking APIs. This integration allows lenders to:

- Confirm account ownership

- Check transaction history

- Ensure the legitimacy of information provided by applicants

5. Watchlist Screening:

From a compliance standpoint, it is always better to identify whom we are dealing with.

Integrating watchlists will help us:

- To identify and prevent any potential frauds.

- Risks by identifying the customer profiles against the watchlists.

- PEP Political exposed people list will also help us to identify high risk customers.

Example: OFAC, EU, Interpole lists

6. Anti-Fraud and Identity Verification Integration:

Preventing fraud is a top priority for lenders. Integration with anti-fraud and identity verification services adds an extra layer of security by confirming the authenticity of borrower identities and detecting potentially fraudulent activities.

Fircosoft and Actimise are some key examples of this.

7. CRM Integration:

Effective customer relationship management (CRM) is essential for building long-lasting relationships with borrowers.

Integrating the loan origination system with a CRM platform can help lenders:

- Manage customer interactions

- Improve communication

- Conduct seamless follow-ups

8. Loan Servicing Platforms:

After loan approval, borrowers enter the loan servicing phase. Integrating the loan origination system with loan servicing platforms can help:

- Facilitate a smooth transition of borrower data

- Ensure that payment processing and customer support continue seamlessly

9. Mobile Application Integration:

Mobile applications brought agility to user behaviour and in today’s M-commerce economy, borrowers expect convenience and accessibility even for buying loans. Integrating the loan origination system with a mobile application can facilitate:

- Quick accessibility to self-assisted LOS

- Easy upload of documents and tracking application status on their smartphones

- Enhanced user experience

10. Analytics and Reporting Tools:

Data analytics support for any application will help CX level personas to take informed decisions. Measuring performance metrics against the available data will help to measure success of the automating any process.

Analytic or Dashboard tools like Power BI or Tableau will help:

- Identify bottlenecks

- Optimize workflows

- Make data-backed decisions

Now, you can clearly see how integrating an LOS with other financial systems, such as credit bureaus, banking systems, and compliance platforms, enables lenders to access borrower’s up-to-date data.

This integration leads to better-informed lending decisions and ultimately reduces the default rates of the financial ecosystem.

To summarize, the integrations and implementations of a Loan Origination System are crucial for enhancing operational efficiency, providing amazing user borrowing experience. To gain the strategic advantages in a competitive market, financial institutions must invest in a creating modern LOS.

Reach out to us at Nitor Infotech to learn more about optimizing your financial workflows with modern technology.