As of 2023, the fintech industry is worth a whopping $179 billion. Yes, you read it right!

Over the past few years, the banking sector has undergone significant changes, mainly due to the rise of the BFSI (Banking, Financial Services, and Insurance) sector. This shift has not only changed how traditional banking works but also created numerous opportunities for businesses.

The BFSI sector covers a wide range of – financial products, services, and risk management expertise, making it a hub for financial innovation.

Great news!

My blog will provide an in-depth exploration of the banking and financial sector, encompassing areas such as:

- Growth of BFSI

- Digital transformation in BFSI

- Overcoming challenges in the BFSI domain

With this blog, you will gain the knowledge needed to make informed decisions that can propel your business beyond conventional benchmarks.

Let’s begin!

The Changing Landscape

Amid the global pandemic’s challenges, the banking and fintech sectors are undergoing a profound transformation as they adjust to the ‘new normal.’

The rapid adoption of digital channels has compelled businesses to navigate a dynamic landscape, meeting evolving consumer demands.

The accelerated digitization of financial services is reshaping how we manage, invest, and transact money. The shift to digital banking and fintech was already underway, but the pandemic’s urgency has expedited it, leading to an unprecedented surge in:

Here are 3 remarkable statistics for you to get a glimpse of the growth of the BFSI arena at present:

- 80% of people use mobile apps for banking or financial services.

- 61% of consumers are open to switching to a digital-only bank.

- 91% of Gen Xers and 79% of baby boomers acknowledge the advantages of digital banking for all generations.

Interesting, right?

Next up, I will be throwing light on how the BFSI is set out to transform the digital terrain.

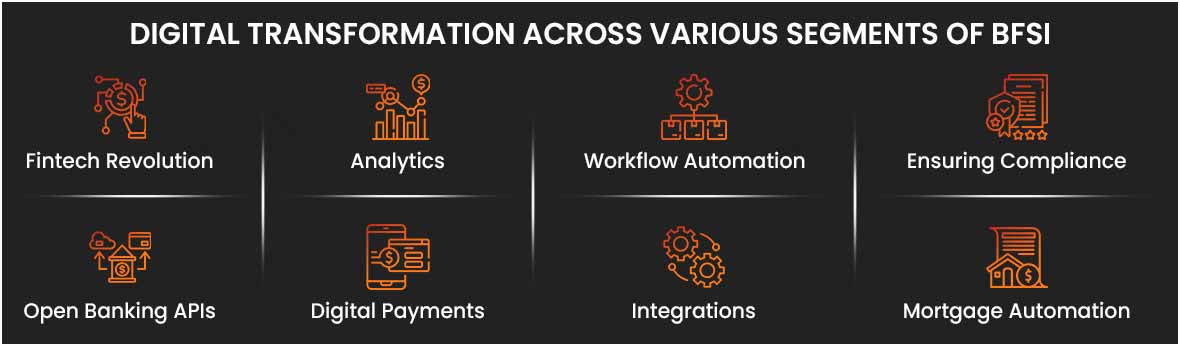

Digital Transformation across Various Segments of BFSI

Here are the key areas where the BFSI sector has been making significant advancements:

- Fintech Revolution: The post-pandemic era has witnessed a remarkable surge in the prominence of fintech companies. These tech-driven startups are at the forefront of delivering cutting-edge, customer-centric financial services by harnessing transformative technologies such as – GenAI, Cloud computing, IoT, and more.

Here are some groundbreaking opportunities that businesses are eager to harness at this moment:

- Peer-to-Peer lending platforms

- Mobile payment solutions

- Account aggregator Platforms

- Hyper-personalized systems

- Open Banking APIs: One of the driving forces behind this transformation is open banking. It allows third-party fintech companies to access financial and transactional data from big banks securely and in a standardized way.

This initiative simplifies the development process, enabling Independent Software Vendors (ISVs) to create applications that seamlessly integrate with multiple banks. It promotes interoperability, making it easier for fintech companies to strategically position their service offerings in the desired market. - Analytics: Creating hyper-connected ecosystems and enhancing customer experiences is essential for making data-driven decisions. Here, analytics plays a pivotal role. It involves the use of data and advanced analytical tools to gain valuable insights into customer behavior, market trends, and operational efficiency.

Through GenAI-driven analytics, financial institutions can now:

- Create highly tailored products and services

- Optimize decision-making processes

- Enhance customer experiences

- Digital Payments: These methods offer unparalleled convenience, enabling swift and hassle-free transactions. Mobile wallets, contactless payments, and peer-to-peer transfers, you name it, it is now possible to manage finances with just a few taps. This transformation has accelerated transaction speed and improved the overall user experience.

- Workflow Automation: This is another cornerstone of digital transformation in BFSI. This involves the use of technology to streamline and optimize various business processes within financial institutions. By automating repetitive and manual tasks, BFSI companies can significantly:

- Improve operational efficiency

- Reduce heavy expenses

- Optimize customer experience

Automating the workflow accelerates time-to-market for new products and services. Thus, ensuring that the BFSI sector remains agile and competitive in a rapidly evolving digital landscape.

- Integrations: These are vital for delivering a seamless and interconnected experience to both customers and financial institutions. In the BFSI sector, multiple services and data sources need to work harmoniously to provide a holistic view of a customer’s financial situation. Through effective integrations, BFSI organizations can – reduce manual effort and enhance the overall performance of their fintech solutions.

- Ensuring Compliance: Compliance is a non-negotiable aspect of the BFSI sector. Digital transformation in this context involves implementing advanced tools and technologies to ensure adherence to regulatory requirements and standards.

Anti-Money Laundering (AML) efforts are a prime example, where transaction monitoring plays a crucial role in detecting and preventing fraudulent activities. Leveraging technologies like GenAI and Natural Language Processing (NLP) aids in reducing false positives and enhancing the effectiveness of AML efforts. Thus, maintaining the sector’s integrity and trust. - Lending and Mortgages Automation: Advanced technologies, such as GenAI and sophisticated analytics, are being used to automate various aspects of the lending process. This includes – assessing creditworthiness, streamlining application processes, and accelerating approvals.

The automation of lending and mortgage operations not only enhances efficiency but also reduces paperwork and administrative burdens for both financial institutions and borrowers.

Note: Navigating the complex world of such BFSI segments requires understanding both the challenges and the ways to overcome them.

Onwards to it!

Overcoming Challenges in the BFSI Domain

Here are the waves of challenges faced by organizations serving the BFSI ocean, along with effective strategies to address each one:

1. Concerns about Security:

Challenge: Safeguarding confidential financial data is paramount, especially in the face of increasing cyber threats. Without a robust security strategy, businesses are always at risk of data breaches and financial losses.

Solution: To solve this problem, businesses should spend on:

- State-of-the-art encryption

- Multi-factor authentication

- Conduct routine security audits

2. Compliance with Regulations:

Challenge: The ever-changing landscape of financial regulations poses a significant challenge, as non-compliance can lead to legal complications and fines.

Solution: To overcome regulatory hurdles, businesses must – employ compliance management systems and stay updated with the latest changes in financial laws. Thus, ensuring they align their practices accordingly.

3. Costs of Digital Transformation:

Challenge: Funding digital transformation initiatives can be financially daunting, but in an increasingly digital world, these investments are necessary for survival and growth.

Solution: To address this challenge, companies should prioritize digital investments strategically, focusing on areas with the most significant potential returns. Further, embracing cloud-based solutions can also reduce costs while enhancing scalability and efficiency.

4. Customer Trust:

Challenge: Establishing and preserving customer trust is vital in a time when data breaches are prevalent. Failing to maintain trust can result in a loss of business and reputation.

Solution: To address this challenge, businesses should maintain transparent communication regarding security measures and data protection policies. Establishing a track record of data security and privacy is crucial in building and preserving customer trust.

5. Competition from Fintech:

Challenge: Traditional financial institutions face stiff competition from nimble fintech startups, making it essential to adapt and innovate to stay relevant.

Solution: To stay competitive, businesses can opt for collaboration with fintech firms, which often leads to mutually beneficial partnerships. Alternatively, organizations can innovate by offering unique services, improving customer experiences, and embracing the agility and technological advancements that fintech startups bring to the industry.

So, the landscape is evolving rapidly, with opportunities for innovative ISVs and fintech companies to create valuable solutions that meet the changing needs of consumers. As the financial world continues to embrace digital transformation, the possibilities for innovation and growth are limitless.

In the next five years, we can expect a period of consolidation where incumbent firms will embrace digital transformation to deepen their capabilities.

Simultaneously, mature fintech companies will explore partnerships to drive disruption and customer-focused innovation.

To tackle shifting threats and build operational resilience we, Nitor Infotech, might just be your right companion in the global BFSI space.

Reach out to us for your next big step!